Money Talk Podcast, Friday Sept. 8, 2017

Podcast: Play in new window | Download

Subscribe: iTunes | Android | Google Play | RSS

Landaas & Company newsletter September edition now available.

Advisors on This Week’s Show

Bob Landaas

Kyle Tetting

Marc Amateis

Dave Sandstrom

(with Max Hoelzl and Joel Dresang)

Week in Review (Sept. 4-8, 2017)

Significant economic indicators & reports

Monday

Markets closed in observation of Labor Day

Tuesday

The Commerce Department reported that factory orders decline in July for the third time in four months and at a large rate of 3.3%, but mostly because of a big increase in commercial aircraft orders in June. Among the less-volatile categories, orders rose, suggesting improved prospects for manufacturers as the global economy grows. A proxy for business investments, which has been lagging for months, rose 1%.

Wednesday

The U.S. trade deficit widened slightly to $43.7 billion in July from $43.5 billion in June, according to the Bureau of Economic Analysis. Exports declined 03%, including a drop in sales of American-made autos abroad. Imports fell 0.2%, including declines in U.S. purchases of foreign oil, autos and industrial supplies. Year-to-date, the trade gap widened by 9.6%, resulting from a 6% rise in exports and a 6.7% increase in imports.

The non-manufacturing sector continued to expand in August for the 92nd consecutive month. The ISM non-manufacturing index rose to 55.3 from 53.9 in July, although it remained below its 12-month average of 56.2. Most of the components in the index grew at a faster pace. The Institute for Supply Management said the index suggests that the overall U.S. economy is growing at a 2.5% annual rate.

Thursday

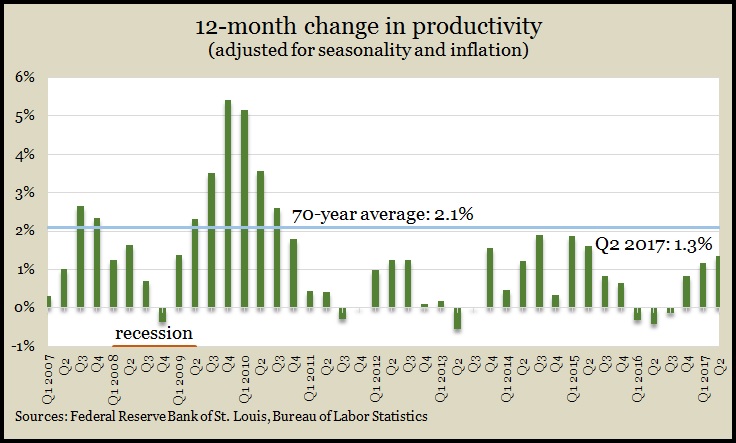

An ongoing concern since the U.S. recovery from the Great Recession is sluggish labor productivity, which continued in the second quarter. The Bureau of Labor Statistics reported that productivity grew at a 1.5% annual rate from April through June. That was an improvement from an initial estimate of 0.9% growth but continues to fall short of past rates. Productivity is key to maintaining the standard of living and raising wages, which fuels economic growth. Year-to-year, productivity increased 1.3% – vs. a 2.1% average since 1947, a level that hasn’t been reached since 2010.

Disruptions from Hurricane Harvey sent the moving four-week average of initial unemployment claims soaring 5.7%, the first increase in the indicator in six weeks and the biggest since 2009. Still, new jobless applications remain 30% below the 50-year average, according to the Labor Department, and continue to point to a persistent reluctance among employers to let workers go. Demand for workers should build pressure for higher wages and increased consumer spending.

Friday

The level of wholesale inventories rose 0.6% again in July gaining at the same rate as sales. The Commerce Department reported that the ratio of inventories to sales ticked up a notch, hovering at a level reached during the Great Recession. Companies have been trying to bring that ratio down to better align supply and demand so they can operate leaner. The ratio climbed to a post-recession peak in January 2016.

The Federal Reserve reported that growth in credit card debt slowed in July, suggesting that Americans were more hesitant about spending. So-called revolving credit expanded by $2.6 billion from June, an annual rate of 3.2%, vs. 5.8% in June. Consumer spending drives about 70% of U.S. economic activity. The bulk of consumer credit – non-revolving credit, including student loans and automotive financing – expanded by $15.9 billion or an annual rate of 6.9%.

Where the Markets Closed for the Week

- Nasdaq – 6,360, down 75 points or 1.2%

- Standard & Poor’s 500 – 2,461, down 15 points or 0.6%

- 10-year U.S. Treasury Note – 2.06%, down 0.1 point

- Dow Jones Industrial– 21,798, down 190 points or 0.9%

Send us a question for our next podcast.

More information and insight from Money Talk

Money Talk Videos

Follow us on Twitter.

Landaas newsletter subscribers return to the newsletter via e-mail.