Short life for new normal

By Bob Landaas

“New normal” did not last long. During and just after the financial crisis, developing nations tended to do better than developed nations. Many developing nations avoided a real estate bubble and collapse and a banking crisis. Those countries had surpluses and citizens without large debts.

The notion of a “new normal” for investors predicted that the emerging economies would lead the world in economic growth into the future. Well, the future lasted five years.

In the last few months, the tide has turned. The developed world is now producing more than the emerging markets. Manufacturers and service companies are reporting growing business in developed countries.

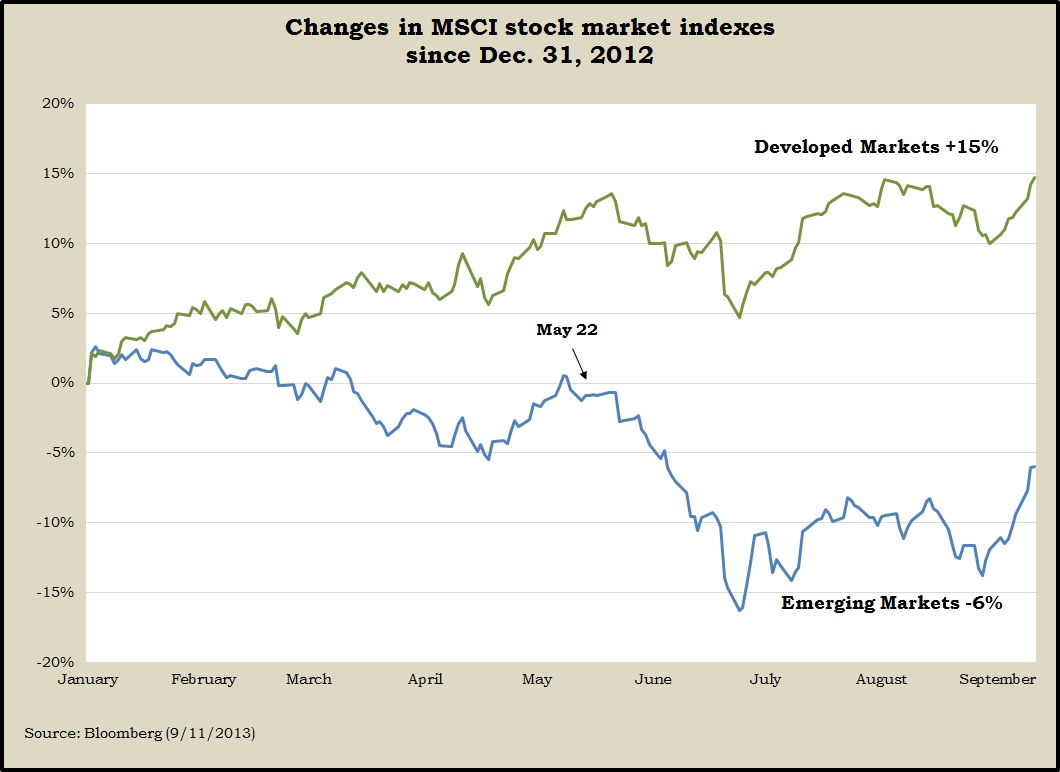

For the first time since mid-2007, the advanced economies of the U.S., Europe and Japan are contributing more than the emerging nations to growth in the $74 trillion global economy. This turnabout is changing world capital flows and is challenging traditional asset allocation assumptions.

Several forces are driving the global shift, including:

- Consumer demand drove the past two U.S. expansions, but has been modest in recent years, meaning slower growth in demand for foreign goods. The latest U.S. expansion has benefited from domestic energy production, which creates demand for U.S.-made equipment.

- Japan is finally growing after years of stagnation. Japan’s economy grew 3.8% on an annualized basis in the second quarter. Prime Minister Shinzo Abe’s expansionary fiscal and monetary policies are working after two decades of deflation.

- The recession in Europe is finally over. The European debt crisis, for now, is under control

- Rising interest rates in the U.S. have squeezed credit in parts of the emerging markets. The Fed’s low interest rates over the last five years sent money pouring into developing nations as investors chased higher yields. Now that trend has reversed as interest rates head higher.

- Growth in Russia, Brazil, India and China is slowing after a run of strong growth.

- Much of the change can be traced to China, the world’s second-largest economy. While still growing at over 7% this year, it is the slowest rate since 1990.

China’s reduced demand for commodities like iron ore, copper and coal has affected Latin America and Southeast Asia. Brazil’s exports of iron ore to China are down, as are Indonesia’s shipments of coal to China, holding those economies back.

In recent years, investors have flocked to emerging markets as low interest rates in the U.S. touched off a global search for yield. The trend reversed this spring as interest rates climbed in the U.S. The Fed tapering is viewed as hurting the emerging markets.

Emerging market stocks fell 12% in June after Fed Chairman Ben Bernanke said the U.S. could start tapering its bond buying as early as September.

The bonds, currencies and stock markets of many developing nations have been hit as investors braced for the Fed tapering. When emerging market currencies fall, dollar-denominated loans largely need to be paid back in dollars. That creates two problems: Paying off dollar loans becomes more costly, and lenders become more skittish and may move to reduce lines of credit.

Now, emerging nations are raising interest rates in an effort to stem an exodus of cash in a trend that threatens to intensify an economic slowdown in the developing world. The relative outperformance by the developed markets has been greater than at any time in 15 years.

Recessions in the U.S. have almost always led to more severe downturns in emerging markets. On the other hand, the U.S. has weathered past storms in the developing world – Mexico in 1994, Asia in 1997, and Russia in 1998 – without going into recession.

Despite federal tax increases and spending cuts and the Fed’s intention to taper its stimulus program, the U.S. economy is surprisingly resilient. Western Europe and Japan are also showing signs of recovery. As a firm, we have a very small exposure to the emerging markets and recently reduced our exposure even more.

As long-term investors, in a global economy, we cannot overlook the developing markets and their potential – especially as their populations of middle-class consumers grow. But the last several months have reminded us that we also should not dismiss the developed countries and the world’s largest economy.

Bob Landaas is president of Landaas & Company.

(initially posted Oct. 1, 2013)

More information and insight from Money Talk