Podcast: Play in new window | Download

Advisors on This Week’s Show

(with Max Hoelzl, Joel Dresang, engineered by Jason Scuglik)

Week in Review (March 16-20, 2026)

Significant Economic Indicators & Reports

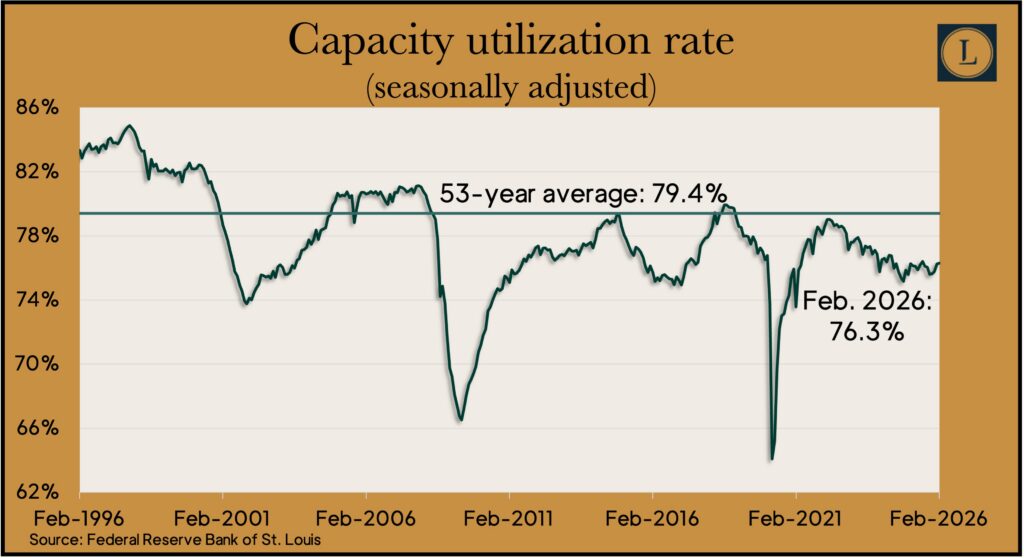

Monday

U.S. industrial production rose 0.2% in February, following a 0.7% gain in January, according to the Federal Reserve. Manufacturing output also increased 0.2%, led by automotive products. In the last year, total production advanced 1.4% while manufacturing rose 1.3%. The capacity utilization rate, considered a leading indicator of inflation, was unchanged in February, staying at 76.3%, well below the long-term average.

Tuesday

Prospects for home sellers brightened slightly in February with a bump up in the pending home sales index from the National Association of Realtors. The trade group said its index rose 1.8% from January and 0.8% from the year before, though it still stood about 28% below the 2001 index, which the Realtors consider to be a normal sales level. The association credited improved affordability for the rise in pending sales. It also said affordability could be threatened by a “sluggish” job market and rising energy costs stemming from the war in Iran.

Wednesday

Wholesale inflation rose more than analysts expected in February with the highest jump in goods prices since August 2023. The Bureau of Labor Statistics said its Producer Price Index rose 0.7% from January. It was up 3.4% from the year before, the most in a year. Excluding volatile prices for food, energy and trade services, the core PPI rose 0.5% from January and was 3.5% higher than the year before.

Demand for U.S. manufactured goods rose in January for the fourth time in six months. The Commerce Department reported that new orders for factory goods grew by 0.1% from December and were 3.5% ahead of their level in January 2025. Gains were led by commercial aircraft orders, which offset declines in automotive and military aircraft. Excluding the volatile transportation category, orders rose 0.4% for the month and 0.6% for the year. Core capital goods orders, a proxy for business investments, rose 0.1% from December and 2.9% from the year before.

As widely anticipated, the policy-making committee of the Federal Reserve Board voted to hold short-term interest rates steady. After a two-day meeting, the Federal Open Market Committee noted that inflation continued to run above the Fed’s 2% target, although the economy appeared to be expanding at a solid pace and the labor market showed little change since the last meeting.

Thursday

The four-week moving average for initial unemployment claims fell for the third time in four weeks to 42% below its average since 1967. The Labor Department report suggested continued reluctance among employers to let workers go. Total jobless claims dropped 3.4% from the week before to just under 2.2 million, which was 0.3% behind the same time in 2025.

The market for new houses sank to its slowest pace in more than three years in January. The annual rate of new residential sales fell nearly 18% from December and was the lowest since October 2022, the Commerce Department reported. As a result, the inventory of unsold new houses rose to a 9.7 months’ supply. The median price for a new house fell 6.8% from the year before to $400,500.

Friday

No major announcements

Market Closings for the Week

- Nasdaq – 21648, down 458 points or 2.1%

- S&P 500 – 6506, down 126 points or 1.9%

- Dow Jones Industrial Average – 45577, down 981 points or 2.1%

- 10-year U.S. Treasury Note – 4.39%, up 0.11 point