File-and-Suspend suspended

By Lisa Lewitzke

The Bipartisan Budget Act of 2015 contains provisions to close loopholes in Social Security, including what has come to be known as the file-and-suspend claiming strategy.

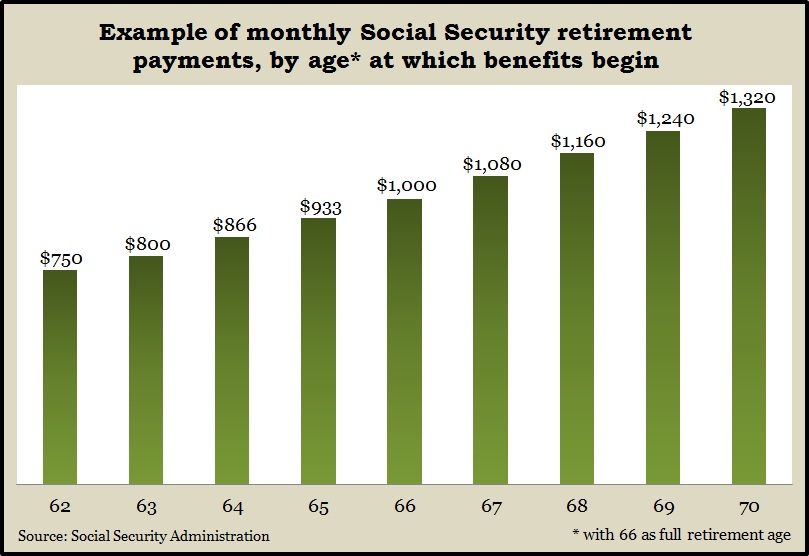

File-and-suspend has made it possible for a married person to file for full retirement benefits at age 66, trigger the spouse’s eligibility for a partial benefit and then suspend the claim up to age 70. Couples have done this to earn delayed retirement credits while also letting the non-claiming spouse or dependent child collect payments worth up to 50% of the claimer’s benefit at full retirement age.

66

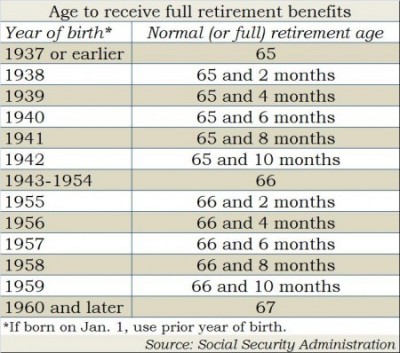

For many, the full age of retirement – 66 – is still the magic number. If you are already 66 or will turn 66 by April 30, 2016, you’re grandfathered in. That means you have a window of a few months to file and suspend and have those partial benefits paid for your spouse or child while you still earn the 8% per year delayed retirement credit.

* Social Security: Know your options, a Money Talk Video with Lisa Lewitzke

* Social Security: Benefits for Spouses

* A Social Security guide on when to start receiving retirement benefits

* Benefits calculators, from the Social Security Administration

However, if you will not be 66 by April 30, 2016 – or if you do not file by that deadline, the option to file and suspend is over. Spouses can still qualify for a partial benefit until they too retire, but if the claiming spouse suspends receiving Social Security, the spousal benefit also stops.

62

A second group of people still has a chance to use the file-and-suspend strategy. If you are 62 or older by Dec. 31, 2015, you still may file for spousal benefits when you turn 66 – as long as your spouse is full retirement age and has claimed Social Security benefits by the April 30, 2016 deadline. This would allow you at age 66 to collect the spousal benefit while you delay claiming your own retirement benefit until age 70, adding 32% to your benefit – 8% for each year you delay.

Where did we get the term “loophole”?

Closing the file-and-suspend loophole has not necessarily made it easier for couples to figure out their best approach to maximizing Social Security benefits. You still have a vast number of choices, based on your individual circumstances. Consider all your options after consulting with your financial advisor or calling the Social Security offices.

Lisa Lewitzke is a registered representative and investment associate at Landaas & Company.

(initially posted Dec. 8, 2015)

More information and insight from Money Talk