Retirement plan: Working longer (or not)

{kind=link}

By Joel Dresang

I turn 60 this year, so it’s safe to say that I’ll retire in the next decade. Or not.

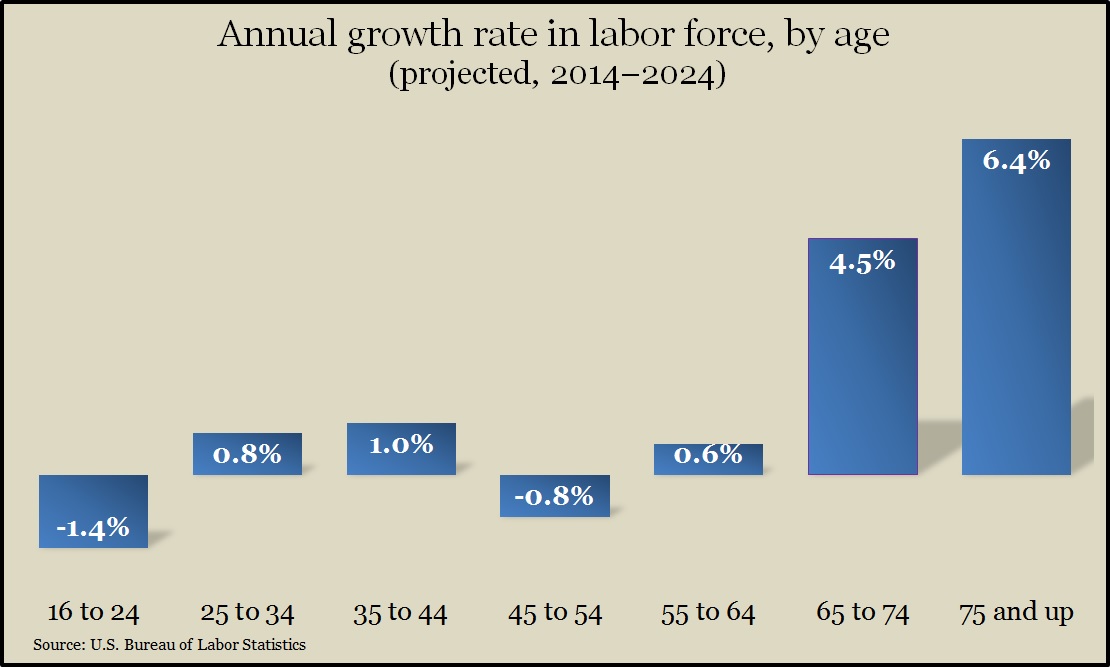

Increasingly, Americans reaching retirement age aren’t retiring. The annual growth rate of people 75 and older is far outstripping every other age group in the labor force. Chalk it up to financial need, improved health, more accommodating employment, any number of factors. The fact is more of us are electing to work longer.

As long as I’m healthy and finding paid work that scratches an itch, that makes me feel that I’m contributing to a better world, I’ll keep working. When my wife doesn’t want me to work anymore, when other interests conflict too much with work and suggest to me that my time is better spent not working, that’s when I’ll consider retiring.

Of course, not all of us will have an option. Annual surveys by the Employee Benefit Research Institute consistently find that about half of retirees left work earlier than they expected, mostly because of circumstances beyond their control, including hardships such as a health problem (41% in the 2017 survey) or changes in their company (26%). For those reasons, we have insurance and investments to support us in retirement.

Why workers plan to delay retirement (could choose more than one):

- Can’t afford to retire (49%)

- Lack faith in Social Security (46%)

- Health care costs (45%)

- Wanting to make sure they have enough money to retire comfortably (44%)

- Higher-than-expected cost of living (41%)

- Need to pay current expenses first (36%)

- The poor economy (32%)

Source: EBRI, 2017 Retirement Confidence Survey

But, if we don’t have the decision made for us, it’s wise to weigh the pros and cons of working longer.

One reason to work longer is to stay active, engaged and purposeful. Many retirees would rather be working. In fact, a recent working paper from the National Bureau of Economic Research reported that 40% of retirees, mostly in their late 60s or 70s, are willing to work again at the same job they left; 20% would take more than a 20% pay cut to return to work with a flexible schedule.

If you keep working, you can accumulate more money for retirement. The Center for Retirement Research at Boston College found that only about 30% of Americans could afford to retire at 62, but if they kept working to 70, 85% could comfortably retire. Among the possible financial benefits from working longer:

- Having more earnings to squirrel away

- Raising the earnings history used for calculating Social Security benefits

- Raising the amount of Social Security payments by delaying to take them

- Shortening the years to be covered by retirement expenses

Likewise, working older can help you reduce medical costs. You can stay on your employer’s health insurance plan longer. And if eligible, you can build a bigger medical care war chest by contributing longer to a tax-advantaged health savings account.

A reason against working longer: Life is short. Some research suggests that retiring early can lead to living longer. To the extent that employment causes stress, takes time away from healthy habits like sleeping and exercising and promotes unhealthy habits like overeating, smoking and alcohol abuse, you can see the connection. Of course, that also entails workers pursuing healthier behaviors in retirement.

According to the Social Security Life Expectancy Calculator, I have 23.5 years left. I know that’s theoretical, but it provides perspective. I have to ask myself how much of that time I want to spend working.

I did some math. If I worked to 70 (at which point, the calculator says, I’d still have 16 years left), my wife and I would have:

- $245,000 more in 401(k) contributions (if I put in the now-maximum $24,500 a year, including catch-up payments for those over 50 – but not including employer matches or investment returns)

- $18,480 a year more in Social Security benefits (the difference between what I am now projected to be eligible for at 62 vs. at 70)

Such figures help provide objective details for what will be a subjective call.

My father retired at 65 and lived a few days past his 88th birthday. That was 23 years in retirement – coincidentally, the same span that Social Security expects me to live yet. But I’m still working.

Maybe I’ll retire in my 60s. Maybe I’ll be in my 70s. Meantime, I’ll keep plugging along, nose to the grindstone – but also ear to the ground and eye on the horizon. Because I know that as long as my wife and I keep saving and investing and watching our expenses, someday we can afford retirement as an option – no matter what happens, no matter how we feel.

Joel Dresang is vice president-communications at Landaas & Company.

(initially posted Feb. 8, 2018)

Learn more When it’s time to retire, by Joel Dresang Retirement 101: Having a plan, a Money Talk Video by Tom Pappenfus

You need a budget, by Tom Pappenfus

Knowing the number, by Brian Kilb

Having the confidence to retire, a Money Talk Video by Art Rothschild

Retirement investing: Where to begin, a Money Talk Video by Kyle Tetting

Send us a question for our next podcast.

More information and insight from Money Talk

Money Talk Videos

Follow us on Twitter.

Landaas newsletter subscribers return to the newsletter via e-mail