Anticipating the return of volatility

By Kyle Tetting

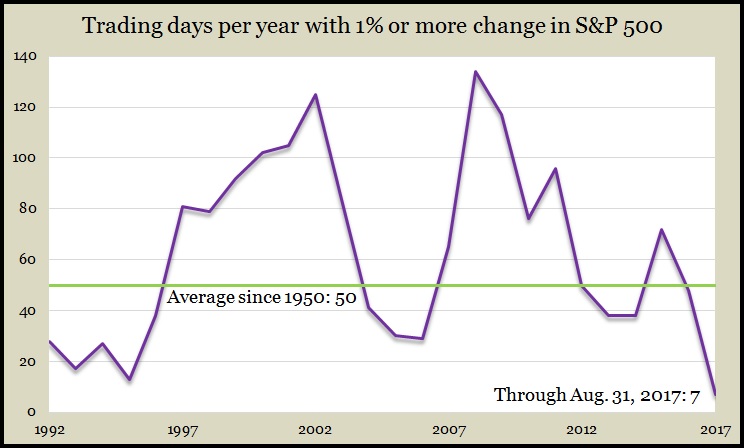

Through eight months of trading in 2017, the S&P 500 has experienced a daily price movement of 1% or more (up or down) just seven times. In 2016, such a feat was accomplished in the first nine trading days of the year. Seven is far below the historical average, accounting for less than 5% of the trading days so far this year. Since 1950, 20% of trading days had a price movement of 1% or more.

While big price moves have been infrequent, the recent ones have accompanied significant U.S. or global events such as rising tensions with North Korea. To interrupt the relative calm has taken a meaningful disruption.

Temporary commotions are ever present. The devastation wrought by Hurricane Harvey provides the most recent example. In addition to the immeasurable impact on the lives of people in and surrounding Houston, there will be a more quantifiable impact on economic growth. Initially at least, the markets have maintained stability, but any big surprise has the potential to add to volatility.

Looking ahead, contentious debate over the U.S. debt ceiling could have the potential to create additional 1% moves in the market. Negotiations over the federal budget and the ability to honor our debts have added to volatility in the past.

Such possible disruptions are likely temporary and may have only a marginal impact on the longer run. A short-term rise in volatility can speak to fear or greed or expectations for the good and bad that might occur, but the general lack of volatility also tells a story.

Coupled with an elevated price-to-earnings ratio, a lack of volatility suggests that strong earnings forecasts are largely baked into the cake. Earnings on the S&P 500 are set to grow nearly 10% over the next four quarters, and investors appear confident in that target. The recent trailing price-to-earnings ratio of 19.4 suggests a market that is no longer cheap. However, the forward P/E of 17.7 highlights expectations for solid growth. Ultimately, markets care more about that forward look and where we are going than the trailing glance back at where we have been.

If investors were overly optimistic, they would be sending floods of cash into stocks, driving prices higher and increasing the potential for wild swings in the market. Instead, $30 billion have left U.S. stock funds over the last 10 weeks, the longest stretch of withdrawals in a decade. Rather than exhibiting irrational exuberance as markets rise and earnings seem to support the current levels, investors have become more complacent in recent months.

Learn more

Risk: How much can you stand? How much do you need? a Money Talk Video with Isabelle Wiemero

Beta: Learning how risky an investment might be, a Money Talk Video with Kyle Tetting

Volatility: What investors should know, a Money Talk Video with Marc Amateis

What investors need to know about volatility, from the Financial Industry Regulatory Authority

Your one-minute guide to stock volatility, from the Financial Industry Regulatory Authority

Coupled with low interest rates, especially in longer-dated bonds, the lack of volatility suggests minimal expectation that the economy will overheat. Investors appear confident in the status quo of modest economic growth without red flags of inflation.

In previous business cycles, low levels of unemployment like we have now tended to drive wages higher and pressure price increases. Wages have gained modestly, but a more nuanced labor market has kept price pressure in check. Additionally, slow global growth the past few years has suppressed commodity prices, also limiting broader inflation.

A recent synchronization of global growth provides some hope that the global economy may be re-accelerating. Global stock markets broadly reflect some optimism but also have avoided irrational exuberance. Investors have contributed more to international stocks but have become overall more conservative in recent months as stocks prices have risen.

Volatility will return – in the form of temporary disruptions from Hurricane Harvey, from the debt ceiling debate or from any number of less foreseeable events. But also, more predictably, wider market fluctuations will come back as the realization of elevated stock prices and the potential for future slower earnings growth catch up with U.S. stocks.

To cope with the eventual resurgence of volatility, a properly balanced portfolio of stocks and bonds – including exposure to accelerating global growth – remains the long-term investor’s most important tool.

Kyle Tetting is director of research and an investment advisor at Landaas & Company.

(initially posted Aug. 31, 2017)

More information and insight from Money Talk

Ask a question for our Money Talk Podcast.

Money Talk Videos

Follow us on Twitter.

Landaas newsletter subscribers return to the newsletter via e-mail